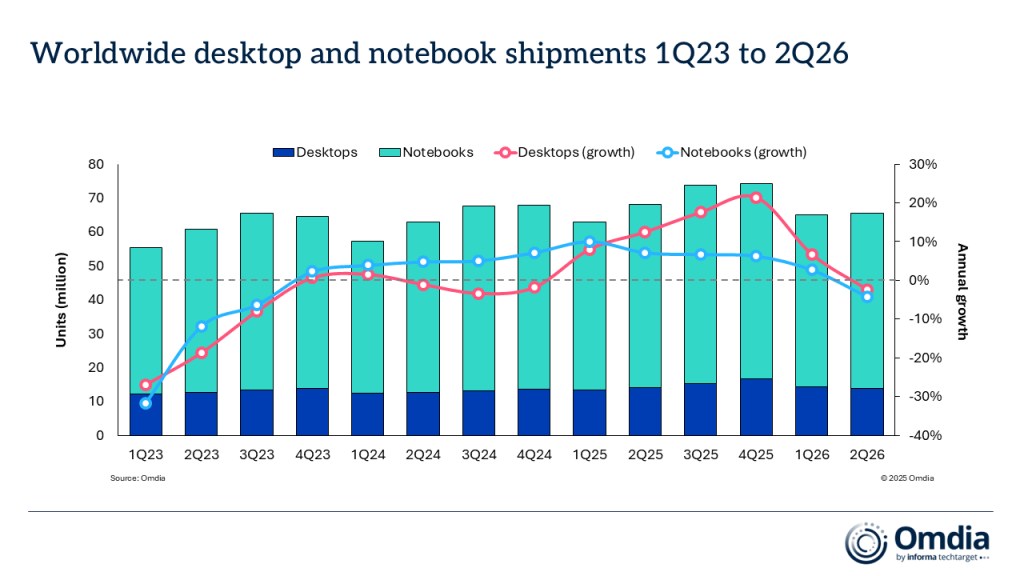

The global PC market weakened in Q2 with shipments falling 3.6 percent year over year to 65.7 million units as vendors faced mounting pressure from rising component costs and tighter supply, according to Omdia.

Even as demand held up in some commercial and refresh-driven segments, the market was weighed down by memory and storage shortages that continued to push prices higher.

According to Ben Yeh, Principal Analyst of Omdia, the sharp increase in memory and storage prices during the first quarter of the year had a significant impact on product pricing in the second quarter.

“It also prompted consumers and IT decision makers to bring forward their PC purchases to mitigate the risk of further price increases. Although sales volumes were maintained at a stable level, the risk of a subsequent downturn remains,” he said.

Lenovo continued to lead the market, retaining the top spot as its scale and broad portfolio helped it stay ahead of rivals.

HP, Dell, Apple, and Asus rounded out the top five, showing that the market is still heavily concentrated among a handful of major vendors despite the overall slowdown.

The latest results highlight how supply dynamics are reshaping competition across the PC industry. Vendors with stronger purchasing power, broader channel reach and more flexible product mix are better positioned to absorb cost increases, while smaller players are likely to feel more pressure on margins and entry-level volumes.

“After the pull-forward activity seen in the first half of the year, signals are now pointing to a period of delayed demand as the true impact of the supply crunch sinks in,” said Ishan Dutt, Research Director of Omdia.